The market is generally segmented by application: Microinverters dominate Residential (where shade is a factor), and high-power String/Central inverters dominate Commercial/Industrial (C&I) and Utility-Scale projects.

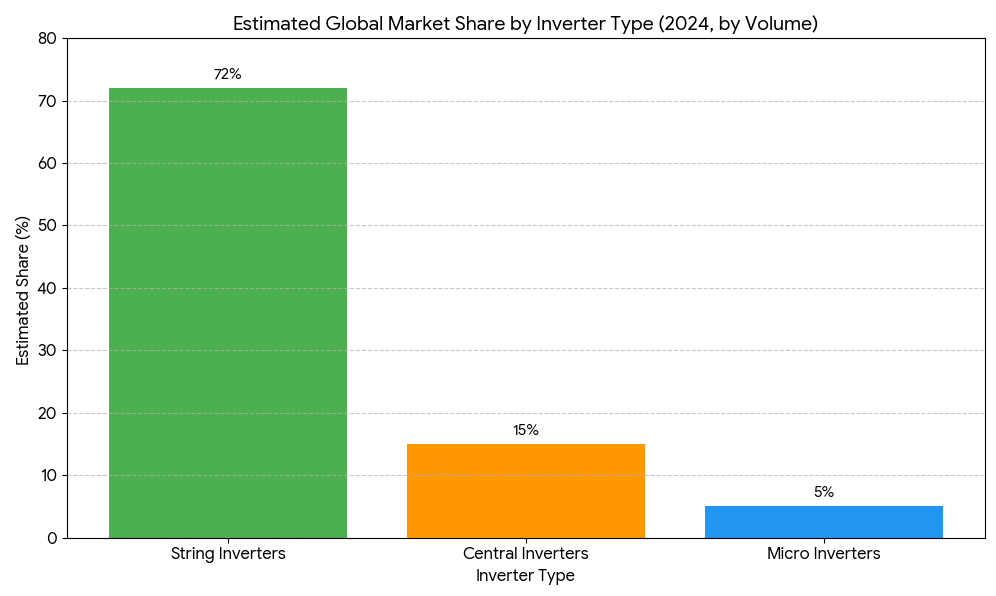

1. Market Share by Inverter Type (Global – by Shipment/Volume)

In 2024, String Inverters are the absolute mainstream technology globally, primarily due to their dominance in large utility projects.

| Inverter Type | Global Market Share (2024 Estimate) | Primary Application |

| String Inverters | ~72% | Residential, Commercial, and Utility-Scale (High-power models) |

| Central Inverters | ~5% – 15% | Utility-Scale (Very large power plants) |

| Micro Inverters | <5% | Residential, Small Commercial (Fastest-growing segment) |

Source: Multiple market analysis reports (Shipments/Volume)

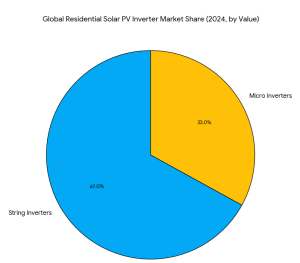

2. Market Share by Application (Residential Segment Focus)

In the residential segment, where microinverters compete directly with low-power string inverters, the market is much closer, with string inverters still holding the overall lead, but microinverters growing rapidly.

| Inverter Type | Residential Solar PV Inverter Market Share (Global Value – 2024) |

| String Inverters | ~67% |

| Micro Inverters | ~33% |

Source: Residential Solar PV Inverter Market Reports (2024)

3. Capacity Range Breakdown

The choice of inverter is heavily dictated by the power capacity of the project.

| Inverter Type | Typical Capacity Range | Dominant Application | Key Market Trend (2024) |

| Micro Inverters | <0.5 kW (per panel) | Residential, Small C&I | Rapidly growing market. Single-phase models dominate residential. |

| String Inverters | 3 kW – 100 kW | Residential, C&I | Single-phase dominates Residential (e.g., <20 kW). Three-phase models dominate C&I (e.g., 60 kW+). |

| High-Power String Inverters | 100 kW – 350 kW | Utility-Scale | Used as an alternative to Central Inverters in large projects (1500V architecture). |

4. US Market Dynamics (North America)

The North American market, particularly the USA, shows a strong preference for microinverters in the residential sector compared to other global regions.

| Region/Segment | Market Dynamics (2024) |

| North America Residential | Microinverters have a very strong presence, often dominating the residential segment by revenue, due to: <ul><li>Strong push for module-level rapid shutdown and safety requirements.</li><li>High levels of partial shading on complex US residential roofs.</li><li>Dominance of key North American microinverter manufacturers.</li></ul> |

| North America C&I / Utility | Central Inverters (e.g., 1.5 MW+) and High-Power Three-Phase String Inverters (e.g., 60 kW+) are the dominant types by installed capacity (MW/GW). |

| Microinverter Market Share (Value) | North America held the largest share of the Microinverter market by revenue (~38%) in 2024, indicating the higher adoption rate of this technology over simple string inverters in residential solar compared to other regions. |

Key Takeaway:

- Globally (Total Capacity): String Inverters (including high-power C&I/Utility models) are the overwhelming leader by volume/shipments.

- USA Residential: The US has the highest adoption rate of Microinverters globally, making them the preferred solution for many homeowners.

- Capacity: Microinverters are solely focused on the small capacity range (<1 kW per unit), while String Inverters span everything from small residential systems up to large-scale utility projects.

Would you be interested in a list of the top 5 global manufacturers for each type of inverter (String vs. Micro) based on 2024 market share?